Climate Insurance leader recognized for innovative property insurance solution that incentivizes resilience in renewable energy assets against increasing natural catastrophe threats

SAN FRANCISCO, October 22, 2024 – kWh Analytics, the market leader in Climate Insurance, has been awarded the Sustainable Insurance Initiative of the Year by InsuranceERM at their Climate and Sustainability Awards. This award marks the second consecutive year kWh Analytics has been honored by Insurance ERM, following their 2023 win for Climate and Sustainability Collaboration of the Year with capacity partner Aspen Insurance.

In 2023 alone, the U.S. experienced 28 natural disasters that caused $1bn or more in damage. In the face of increasing climate risks, exposed energy assets, such as solar, wind, and battery storage, require resilience against these perils to stay online. Renewable energy assets that are ‘resilient’ are specifically designed to withstand regional exposures, utilizing equipment tailored to local conditions. These projects actively prevent exposure to risks through proactive measures such as advanced monitoring systems, strategic siting, and robust maintenance protocols. As natural catastrophes become more frequent and severe, insurers and asset owners alike are recognizing the urgent need for solutions that not only protect investments but also encourage the development of more clean energy. kWh Analytics’ approach directly addresses this growing industry concern by incentivizing and rewarding these resilience measures.

“By combining our unparalleled data, underwriting insights, and deep industry relationships, we’re not just assessing risk – we’re actively incentivizing resilience and sustainability in renewable energy projects,” said Jason Kaminsky, CEO of kWh Analytics. “We’re honored to be recognized by InsuranceERM and our peers for our commitment to push the boundaries of what’s possible in climate insurance.”

Launched in 2023, kWh Analytics’ property insurance solution for renewable energy assets has already expanded capacity limits and secured partnerships with five of the top ten global (re)insurance companies. The program leverages a proprietary database of over $100B worth of renewable energy loss data to conduct precise risk assessments and make informed underwriting decisions.

The program’s unique pricing model incentivizes asset owners to implement climate-resilient practices. A recent case study demonstrated that a utility-scale solar project in hail-prone Texas achieved a 72% decrease in their property insurance natural catastrophe rate by implementing strong hail resilience measures, such as stowing panels against hail and using thicker, heat-tempered glass panels.

The continued growth of the renewable energy industry relies on collaboration across all stakeholders. By incentivizing resilience, kWh Analytics is playing its part alongside resilient equipment manufacturers, diligent operations and maintenance providers, and forward-thinking asset owners. Together, these stakeholders are creating a more sustainable future and accelerating the transition to clean energy.

ABOUT KWH ANALYTICS

kWh Analytics, a leading Climate Insurance provider, underwrites property insurance and revenue firming products for renewable energy assets. Our proprietary database of 300,000+ zero-carbon projects and $100B in loss data fuels advanced modeling and insights, enabling precise underwriting decisions. This data-driven approach incorporates resiliency measures in risk evaluation, promoting sustainable practices in the renewable energy sector.

Trusted by five of the top ten global (re)insurance carriers, we’ve insured over $30 billion in assets to date. Our tailored solutions further our mission of providing best-in-class Insurance for our Climate. Recognized by InsuranceERM Climate and Sustainability Awards, kWh Analytics continues to pioneer in the renewable energy insurance sector.

Geoffrey Lehv, Head of US Accounts for kWh Analytics, joins the Crossroads podcast to discuss the role of insurance in the energy sector and how the industry is innovating to appropriately allocate risk.

Lehv speaks to how kWh Analytics has grown its business from handling risk transfer in the project finance sector to boosting access to financing, enhancing financing and supporting innovation.

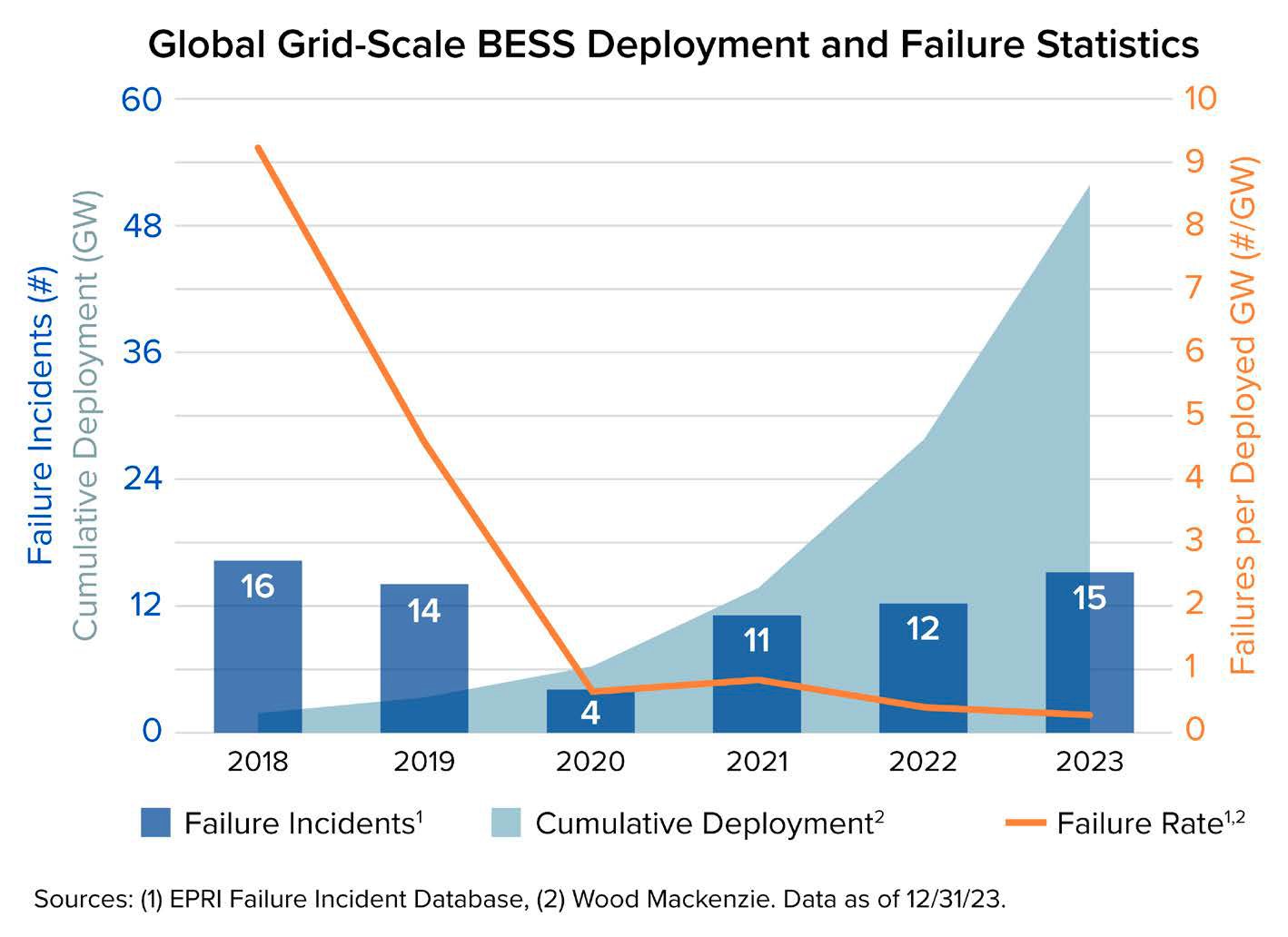

The energy landscape is undergoing a profound transformation, with Battery Energy Storage Systems (BESS) at the forefront of this change. The BESS market has experienced explosive growth in recent years, with global deployed capacity quadrupling from 12 GW in 2021 to over 48 GW in 2023. These sophisticated systems are revolutionizing how we generate, distribute, and consume electricity, offering unprecedented flexibility and efficiency to power grids worldwide.

The trajectory of BESS growth shows no signs of slowing. According to Lloyd’s article in the 2024 Solar Risk Assessment, the industry is poised for a staggering 13-fold expansion, with an additional 181 GW either planned or under construction. This surge is driven by several key factors, capturing the attention of developers and investors alike. The intermittency of renewable energy sources like wind and solar power has created a pressing need for storage capabilities to balance irregular supply with demand. BESS offers crucial grid stabilization services and enables the delivery of more clean energy.

However, with these opportunities come significant challenges. The rapid growth of the BESS industry has outpaced the development of comprehensive safety standards and regulations. The technology itself, while advancing quickly, still faces issues related to energy density, cycle life, and overall performance. Perhaps most critically, BESS installations face a unique risk in the form of thermal runaway events, which can lead to fires and explosions if not properly managed.

Battery chemistry plays a crucial role in both the performance and risk profile of BESS. Lithium Iron Phosphate (LFP) has become the standard for commercial-scale energy storage due to its balance of cost, environmental impact, and safety characteristics. However, other chemistries like traditional lithium-ion, lead-acid, and flow batteries each offer different advantages and challenges depending on the specific application and use case.

Insuring BESS installations presents unique challenges due to the novelty of the technology and the potential for catastrophic events like thermal runaway. However, insurance is not just a cost of doing business—it’s an enabling form of capital that’s critical for the continued growth and adoption of BESS technology. Understanding how to protect these assets effectively is key to securing favorable insurance terms and, by extension, unlocking the financing necessary for new projects. Delving into the intricacies of BESS risks and mitigation strategies may help shed light on how asset owners, developers, and insurers can work together to foster a more resilient and insurable BESS industry, ultimately supporting the transition to a cleaner, more sustainable energy future.

Thermal Runaway: The Critical BESS Safety Challenge

The growth of global installed capacity of utility-scale BESS has naturally led to increased scrutiny of asset safety, particularly in light of high-profile fire incidents that have garnered significant media attention. However, it’s important to note that despite these incidents, the overall rate of failures has decreased sharply. When failures do occur, they are often attributed to a phenomenon called thermal runaway.

Figure 1: Global Grid-Scale BESS Deployment and Failure Statistics

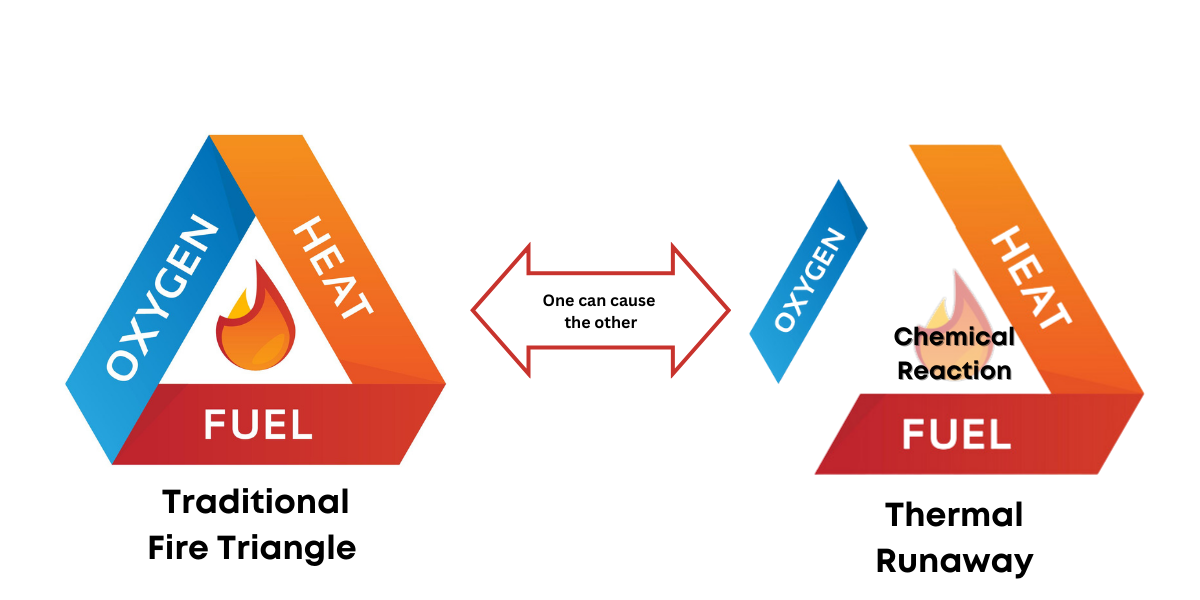

Thermal runaway occurs when a battery cell enters an uncontrollable, self-heating state. This process can rapidly escalate, potentially affecting neighboring cells and leading to a cascading failure across the entire system, often causing fire, explosion, and the release of toxic gases. It’s crucial to understand that thermal runaway in lithium-ion batteries differs significantly from conventional fires. While conventional fires are sustained by fuel, heat, and oxygen[3], and can be extinguished by removing one of these elements, thermal runaway does not require oxygen. Instead, it is fueled by an internal chemical reaction that can continue without oxygen or visible flame.

Figure 2: The ‘traditional’ fire triangle and its relationship to Thermal Runaway

To fully grasp the complexity of thermal runaway, it’s essential to understand its progression. The process typically unfolds in three distinct phases, each with its own characteristics and challenges:

Initial Instability: A voltage or temperature instability occurs, and the cell begins emitting gases.

Internal Short Circuit: The voltage drops to zero as internal cell materials fail, and the anode and cathode experience a direct internal short. The stored electrical energy in the battery flows through this short, causing temperatures to spike as high as 300-600°C. Importantly, visible flame may or may not occur at this stage.

Consumption of Cell Materials: As the internal materials of the cell are consumed, the thermal runaway event can transition to consuming the cell’s encasing materials such as the electrolyte, polymers, and plastics surrounding the cell. The gaseous emissions at this stage are consistent with a plastic fire.

Understanding what triggers thermal runaway is equally important as recognizing its phases. Several factors can initiate this dangerous process:

Electrical Abuse: Overcharging or over-discharging batteries can lead to undesirable electrochemical reactions. When batteries are charged beyond their specified voltage range, it can result in electrolyte decomposition on the cathode surface, increasing battery temperature. Excessive lithium-ion migration during overcharging can destabilize the cathode, potentially initiating thermal runaway.

Mechanical Abuse: External damage to Li-ion batteries, such as impacts, indentations, or punctures, can compromise the integrity of the cell. If the casing is damaged, air can enter and react with the active components and electrolyte, generating heat. Severe internal damage can also lead to short circuits within the cell.

Internal Failures: Manufacturing defects or degradation over time can lead to internal short circuits, generating enough heat to initiate thermal runaway. These failures are particularly challenging, as they are hard to detect with external inspections.

Once thermal runaway begins in a single cell, it can quickly escalate into a cascading failure affecting neighboring cells and potentially the entire BESS installation. The heat generated by the failing cell can raise the temperature of adjacent cells, pushing them into thermal runaway as well. Additionally, failing cells can release flammable and toxic gases, further exacerbating the situation.

The consequences of a thermal runaway event in a large-scale BESS can be catastrophic. High-profile incidents have resulted in significant property damage, extended system downtime, and in some cases, injuries to first responders. These events not only pose immediate safety risks but also have broader implications for public perception and regulatory scrutiny of BESS technology.

Despite these challenges, it should be noted that the BESS industry has made significant strides in understanding and mitigating the risks associated with thermal runaway. As manufacturers, operators, and regulators gain more experience with large-scale BESS deployments, they have been able to identify common failure modes and develop more effective mitigation strategies.

Risk Mitigation Strategies and Best Practices

The BESS industry’s approach to risk mitigation, particularly regarding fire protection and suppression, has undergone a significant evolution over the past eight years. This journey reflects the industry’s growing understanding of the unique challenges posed by large-scale battery installations.

The landscape changed dramatically following a series of fires in Korea in 2017 and 2018. These incidents prompted a shift towards gaseous fire suppression systems in containerized units and dedicated BESS rooms. The theory was simple: remove oxygen from the environment to suppress fires effectively. However, the limitations of this approach became apparent with the APS Surprise, Arizona event in 2019, where quelled fires reignited upon the reintroduction of oxygen into the system.

In response to the Surprise, AZ incident, many fire departments and authorities began requiring water-based fire protection systems for BESS installations. Yet, several events since 2020 have revealed flaws in relying solely on water-based systems, particularly in remote locations where water availability can be limited.

Today, the industry has come full circle, returning to an approach that echoes the pre-2017 era but with pivotal enhancements, specifically the mandatory inclusion of Battery Management Systems (BMS). These systems are the nerve centers of modern BESS installations, playing a role in both performance optimization and safety management. BMS provides sensing and control of critical parameters, and importantly trigger protective or corrective actions if the system is operating out of the norm. These parameters include battery module over or under voltage, cell string over or under voltage, battery module temperature, temperature signal loss, and battery module current. In the event of any abnormal condition, the BMS will first raise an information warning and then trigger a corresponding corrective action should certain levels be reached.

While the Battery Mangement System is an essential component of BESS safety, a comprehensive approach to risk management includes several other best practices:

Spatial Separation and Explosion Relief: Effective explosion relief systems require design conformance to NFPA Standards and sufficient spatial separation between containers or structures to avoid collateral damage. The standard minimum distance for non-sprinklered LFP containers is 6 feet.

Multi-Layered Approach to Fire Protection: While the emphasis is on prevention, many installations still incorporate fire suppression systems as a last line of defense. This may include a combination of gaseous suppression, water-based protection, and emerging coolant-based systems.

Adherence to Evolving Standards: Compliance with applicable fire and building codes provides a basis for resilience. As these standards continue to evolve, BESS operators must stay informed and adapt their systems accordingly.

Conforming to these best practices is not just a matter of regulatory compliance; it’s necessary for the long-term viability and growth of the BESS industry. As energy storage becomes increasingly central to our power infrastructure, the safety and reliability of these systems directly impact public trust, regulatory support, and investor confidence. BESS operators who prioritize these best practices not only mitigate their own risks but also contribute to the overall resilience and reputation of the industry. Moreover, as insurers and regulators scrutinize BESS installations more closely, those adhering to best practices are likely to find themselves in a more favorable position for insurance coverage and regulatory approval.

Beyond Compliance: Proving Resilience to Insurers

For battery storage asset owners, navigating the insurance landscape can be as complex as the technology itself. Insurers are looking beyond mere compliance; they seek evidence of a comprehensive, proactive approach to risk management. The following areas are critical for positioning BESS projects favorably in the eyes of underwriters:

Prove Preparedness

Insurers want evidence of active prevention rather than not just reaction to potential issues, but actively preventing them. This starts with your Battery Management System (BMS). Asset owners should be prepared to demonstrate how the BMS goes beyond basic monitoring, showing its capability to detect subtle anomalies that might precede a thermal runaway event and, crucially, how it autonomously implements corrective actions.

Remote monitoring is no longer a luxury—it’s a necessity. Insurers are looking for systems that provide real-time, granular data on battery performance. The monitoring setup should allow for rapid intervention before small issues become major incidents.

Design for Safety

The physical layout of BESS installations significantly impacts risk assessment. Insurers are particularly interested in spatial separation between enclosures. While a minimum of 8 feet (already more conservative than NFPA code standards) is often cited as a benchmark, asset owners should be prepared to justify their chosen configuration based on specific risk assessments.

Fire suppression systems remain critical, but the approach must be tailored to the specific installation. Asset owners should be ready to explain the rationale behind their chosen system—whether gaseous, water-based, or an emerging technology—and how it’s optimized for the specific setup and location.

Commitment to safety should extend beyond technology. Insurers look favorably on projects that engage experienced O&M providers familiar with regional specifics. Demonstrating coordination with local fire departments, including specialized training programs tailored to the BESS installation, is important.

Chemistry Considerations

Battery chemistry choice significantly impacts the risk profile. While Lithium Iron Phosphate (LFP) batteries are generally viewed favorably due to their stability, other chemistries may be beneficial depending on the use case.

Comprehensive Documentation

Thorough documentation is crucial. Insurers like to see:

Detailed site plans

Comprehensive BMS specifications

Fire suppression system details

Testing certifications

Maintenance protocols

Staff training programs

This information should be contextualized to demonstrate how each element contributes to the overall risk mitigation strategy.

The Path Forward

The BESS industry stands at the cusp of a transformative era, with rapid growth driven by technological advancements and the pressing need for sustainable energy solutions. As deployments scale up, emerging technologies like artificial intelligence and advanced data analytics are reshaping how we approach battery management and risk mitigation.

This technological revolution, however, must be balanced with a thorough understanding of the risks inherent to BESS. The industry’s future hinges on our ability to build resilience into every aspect of BESS design, operation, and insurance. From innovative battery chemistries to sophisticated monitoring systems, each advancement plays a crucial role in enhancing safety and reliability.

As insurers and operators gain more experience and data, we’re seeing a shift towards more nuanced risk assessments and tailored insurance solutions. In this evolving landscape, brokers play a pivotal role. They should be proactively seeking detailed information and documentation from their clients and marketing these accounts across the insurance market. Not all insurers are equipped to make price adjustments based on resilience measures, making it crucial for brokers to work with those who have their arms around this risk class.

Looking ahead, there is reason for optimism for the battery energy storage. The industry has shown adaptability in the face of adversity, and the collaborative efforts between developers, brokers, and insurers are paving the way for safer projects. Carriers are only likely to become smarter and more comfortable with storage as the technology matures. By continuing to prioritize resilience, embracing innovative risk management strategies, and communicating with the insurance markets, we can ensure that BESS continues to play a vital role in our clean energy future, powering us toward a more sustainable and secure energy landscape.

San Francisco, CA – September 23, 2024 – kWh Analytics, a leading provider of Climate Insurance for renewable energy assets, is excited to announce a new, $2.4M partnership with the U.S. Department of Energy Solar Energy Technologies Office (SETO) through the Materials, Operation, and Recycling of Photovoltaics (MORE PV) Funding Program. This partnership aims to develop innovative approaches to solar PV resilience, focusing on introducing asset resilience measures against natural catastrophes earlier in the asset development lifecycle.

The increasing severity and frequency of damage-causing natural catastrophes, such as hail, hurricanes, and floods, pose a significant threat to solar assets, putting clean energy goals at risk. In today’s environment, developers lack the tools they need to make informed decisions on how to design, build, and operate more resilient facilities; kWh Analytics’ project aims to produce tools to help asset developers address the specific perils their assets are exposed to at every stage in the project lifecycle.

“This award is a testament to both the long-standing partnership between kWh Analytics and the U.S. Energy Department, and our organization’s commitment to advancing the energy transition,” said Jason Kaminsky, CEO of kWh Analytics. “Our deep industry knowledge and unparalleled data give us unique insight into climate-resilient design, construction, and management of renewable energy assets – knowledge that we apply to our underwriting decisions and risk assessment. ”

The funding will support several key initiatives, including aggregating real-world renewable energy physical loss data and developing standardized best practices. Project partners include the National Renewable Energy Lab, known for resilience best practice research; DNV, a prominent independent engineer; and lender’s consultant STANCE Renewable Risk Partners.

In the context of solar energy, resilience refers to an asset’s ability to withstand, adapt to, and quickly recover from disruptions caused by extreme weather events or other natural disasters. This includes features such as reinforced mounting systems, hail-resistant panels, and advanced monitoring and response systems. By focusing on resilience, the solar industry aims to ensure the long-term viability and reliability of clean energy infrastructure.

kWh Analytics is committed to connecting researchers and industry experts to the insurance market to foster a collaborative environment for sharing best practices and knowledge. Each year, kWh Analytics publishes its ‘Solar Risk Assessment,’ recognized as the solar industry’s leading report on the evolving landscape of solar generation risk. The report has become a staple read for the solar insurance industry, serving as a guide for investors who recognize the importance of allowing data-based insights inform the deployment of capital. The MORE PV research award is a further opportunity to work alongside industry experts to advance resiliency measures to mitigate solar generation risks and collectively support the energy transition.

kWh Analytics was selected as a part of the SETO Materials, Operation, and Recycling of Photovoltaics (MORE PV) Funding Program. MORE PV projects address challenges associated with the rapid deployment of PV systems in the United States, including the increasing demands on PV materials, system operation and maintenance, and recycling. kWh Analytics is one of several project partners that will support technology improvements to reduce these challenges with a holistic view of all stages of the PV lifecycle—from the material needs and installation to operation and end of life.

ABOUT KWH ANALYTICS

kWh Analytics is a leading provider of Climate Insurance for zero-carbon assets. Utilizing their proprietary database of over 300,000 operating renewable energy assets, kWh Analytics uses real-world project performance data and decades of expertise to underwrite unique risk transfer products on behalf of insurance partners. kWh Analytics has recently been recognized on FinTech Global’s ESGFinTech100 list for its data and climate insurance innovations. Property Insurance offers comprehensive coverage against physical loss, with unique recognition and consideration for site-level resiliency practices, and the Solar Revenue Put production insurance protects against downside risk and unlocks preferred financing terms. These offerings, which have insured over $30 billion of assets to date, aim to further kWh Analytics’ mission to provide best-in-class Insurance for our Climate. To learn more, please visit https://www.kwhanalytics.com/, connect with us on LinkedIn, and follow us on X.

About the Solar Energy Technologies Office

The U.S. Department of Energy Solar Energy Technologies Office supports research, development, demonstration, and technical assistance to improve the affordability, reliability, and domestic benefit of solar technologies to support an equitable transition to a decarbonized energy sector. Learn more at energy.gov/solar-office.

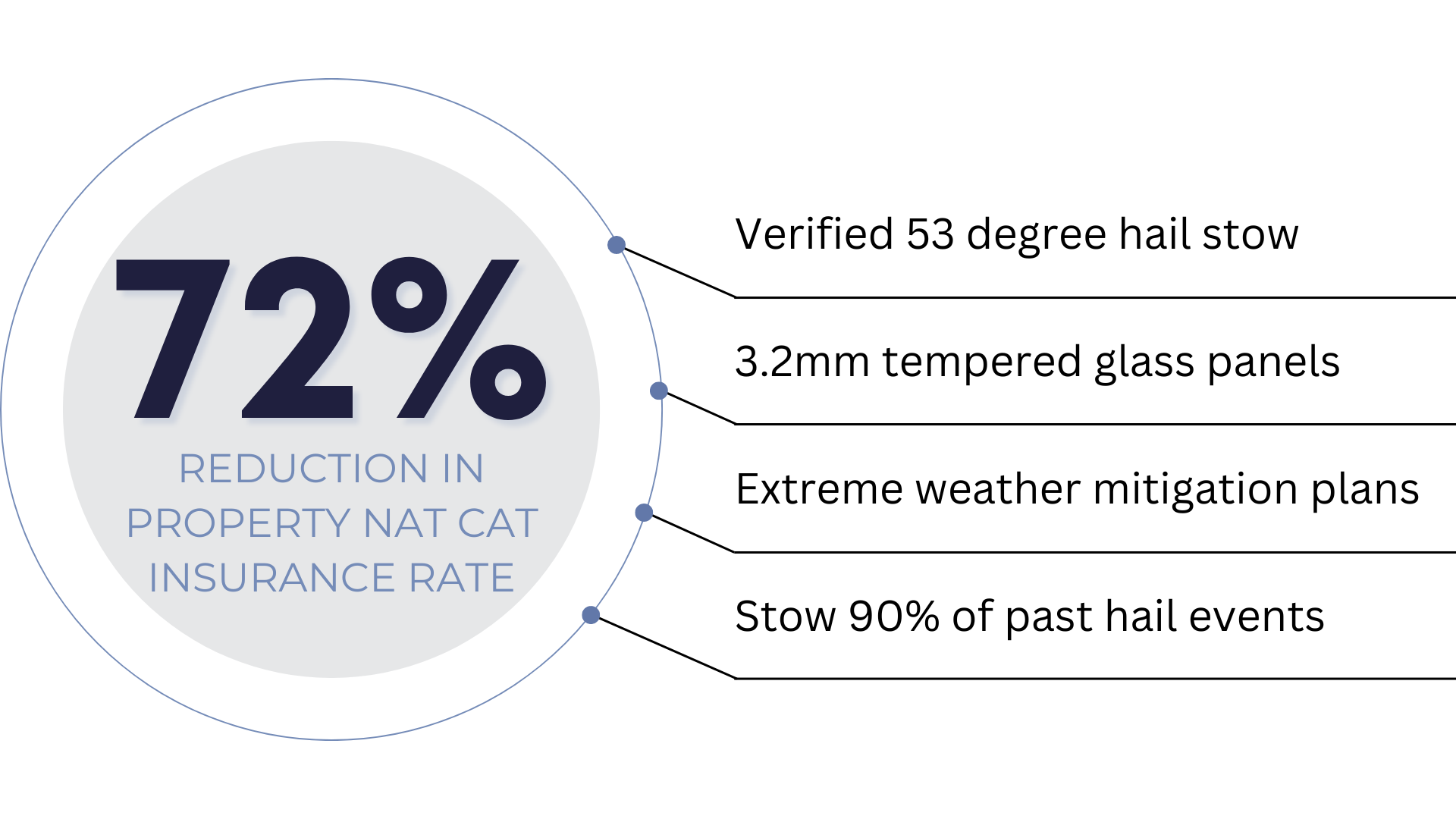

A utility-scale solar developer saw a 72% natural catastrophe rate reduction for employing resilient site design and operation

The Challenge

In a market where insurance rates for renewable energy projects are climbing, especially in hail-prone regions, asset owners face increasing pressure to protect their investments. This is particularly true in North Central Texas, where one developer sought coverage for their 140MW solar project valued at $100MM in a high hail risk area.

The Solution: Proactive Resilience Measures

The developer implemented a comprehensive strategy to harden their asset against natural catastrophes:

Physical Hardening:

Installed 3.2mm tempered glass solar panels

Used high-quality components across modules, inverters, and tracking systems

Operational Protocols

Implemented a verified 53-degree hail stow angle

Developed comprehensive extreme weather mitigation plans

Executed proactive stowing for over 90% of past hail events

Proving Resilience

What set this developer apart was the evidence of resilience provided to their brokers and carriers with thorough documentation and proactive approach:

Provided photographic evidence of the hail stow angle

Submitted stow logs for recent months, demonstrating consistent operational implementation

Incorporated resilience planning from the project’s design phase

The Result: Substantial Insurance Savings

kWh Analytics underwriters, recognizing the developer’s commitment to resilience, were able to offer a 72% reduction in the natural catastrophe insurance rate for this project—this significant saving directly resulted from the developer’s investment in physical hardening and operational measures.

The Takeaway

By combining physical asset improvements with smart operational protocols, developers cannot only protect their assets but also secure substantial insurance savings.

kWh Analytics values sponsor resilience measures and they do impact our premiums. We work directly with developers and brokers to ensure that investments in resilience translate into tangible financial benefits.

For more information on how your resilience measures can be factored into your insurance program, ask your broker for a kWhote.

Brokers Respond to kWh Analytics’ 2024 Solar Risk Assessment: Key Takeaways and Insights

By Jason Kaminsky, CEO kWh Analytics

The 2024 Solar Risk Assessment report has sparked a lively discussion among industry professionals about the evolving landscape of renewable energy insurance. To facilitate a deeper exploration of the report’s findings, our team at kWh Analytics convened its inaugural Broker Council, bringing together leading brokers specializing in solar and renewable energy insurance. The council provided a platform for these experts to share their reactions to the report, discuss the implications for the industry, and identify actionable takeaways for stakeholders. The Broker Council meeting was hosted by geoff lehv of kwh analytics and consisted of the following participants: Rob Battenfield (AmWINS), Todd Burack (McGriff), Mike Cosgrave (Renewable Guard), Stephanie Coveney (Brown & Brown), Matt Giambagno (Marsh), Sara Kane (CAC Specialty), and Alex Morris (WTW).

Emphasizing Equipment Resiliency in the Face of Extreme Weather

The brokers at the council agreed with the Solar Risk Assessment report’s emphasis on the growing impact of extreme weather events on renewable projects. Todd Burack from McGriff highlighted the importance of technological resiliency, stating, “Most of the recent discussions I’ve been a part of with asset owners have gravitated towards technological resiliency. Modeling plays a tremendous role, but I think many carriers who’ve written some of the marquee (hail) losses from the past few months will agree that the losses occurred on projects that actually modeled quite favorably. Many carriers are still playing ‘modeling catch-up,’ and the nature of extreme weather is that it’s hard to predict.”

Takeaway: To mitigate the risks posed by extreme weather events, project stakeholders should adopt a comprehensive approach to risk management that includes careful partner selection, investment in defensive equipment capabilities, and the development and implementation of well-defined operational procedures.

Challenges for Pure Play Developers Sara Kane from CAC emphasized the challenges faced by pure play developers, those looking to ‘flip’ assets to long-term owners, in understanding and managing insurance risks: “The biggest opportunity for better site resilience that we see is for pure play developers to incorporate insurance considerations in early-stage project development. These players, who will likely sell prior to construction, have not historically had a way to understand how the insurance market values different resilience measures in their underwriting decisions, and yet those decisions – site selection, equipment choice and design – will impact insurance costs and ultimately matter in their project sale. We as an industry would be collectively better off if all the projects coming to market had the benefit of insurance diligence at the early-stage development phase, as projects would likely be more resilient.”

Takeaway: Developers who plan to sell their projects should be well-versed in potential insurability challenges and subsequent impacts on project sales. Developers who fail to adequately address natural catastrophe related risks may find it more difficult to secure favorable sale terms or even struggle to find buyers altogether.

Navigating the Risks and Opportunities of Battery Energy Storage Systems (BESS)

The Solar Risk Assessment report’s coverage of the risks and opportunities associated with the rapid growth of Battery Energy Storage Systems (BESS) prompted a thoughtful discussion among the brokers. Commenting on the Lloyd’s article citing that the global battery storage industry is poised for 13x growth over the next few years, Mike Cosgrave from Renewable Guard shared insights from their in-house battery storage engineer, noting that battery construction and integration was the cause for 36% of system failures. “We’re seeing a lot of project delays due to a lack of transformers,” Cosgrave added. “If we’re getting cells from China and overseas, replacing those in a few years might be a challenge if tariffs are in play. While there may be some headwinds to achieve 13x growth, the prospect of achieving that milestone is very exciting for the industry.”

Stephanie Coveney from Brown & Brown added that there are still quite a few unknowns about BESS systems that can make insurance pricing and underwriting difficult: “We still don’t have consensus on how battery units should be spaced, and carriers are setting their own terms, some asking for 25 feet between units, and some manufacturers recommending a small gap around 3 feet between units. There are still a lot of questions to answer in this space.”

Takeaway: As the BESS market continues to expand, project developers should ensure that their projects are designed and operated following industry best practices, with a particular focus on fire safety, thermal management, and system integration.

Exploring Alternative Risk Transfer Solutions

The brokers at the council expressed interest in the Solar Risk Assessment report’s findings on the growing popularity of alternative risk transfer solutions, such as parametric insurance and captives, in response to rising traditional insurance premiums. In the context of renewable energy insurance, parametric solutions offer an alternative to traditional indemnity-based policies. Parametric insurance provides predetermined payouts based on the occurrence of specific triggering events, such as a hurricane of a certain category or a hail event with hailstones exceeding a specified diameter, rather than the actual loss incurred by the insured project.

Alex Morris from WTW shared his perspective on the increasing viability of parametric solutions: “I think parametrics are getting close to being viable when they were simply not an option just four or five years ago. Excess catastrophe coverage is becoming extremely expensive, and now all types of solutions are back on the table. Sponsors are starting to see the value in higher, upfront investments into resilient equipment and defensive measures to protect their assets for the long term.”

Matt Giambagno from Marsh shared his view that “parametric policies are still a gamble. It’s an untested market, unlike traditional property insurance. It’s hard to gauge the likelihood of extreme weather events, but the continuous price increase of excess natural catastrophe coverage is making alternative solutions like these more attractive.”

Takeaway: As the cost of traditional insurance continues to rise, project developers and asset owners are exploring alternative risk transfer solutions.

Addressing Variability in Pricing and Terms

The Solar Risk Assessment report highlighted the variability in pricing and terms across the renewable energy insurance market, a finding that resonated with the brokers at the council. In response to an article by kWh Analytics highlighting that the use of industry-standard modeling assumptions in pricing can lead to an over- or under-estimation of solar risk, Rob Battenfield from Amwins noted, “The variability of pricing and terms and conditions widely varies across the broking world. We see this a lot when we are placing excess severe convective storm policies (hail) for example – different programs can have widely different results. Working with brokers and underwriters that are knowledgeable in the space is a recipe for success, and can make or break a project from the insurance perspective.”

Takeaway: To navigate the complex and varied landscape of renewable energy insurance, project sponsors should partner with brokers and underwriters experienced with renewables early in the project planning process.

The brokers’ reactions to the 2024 Solar Risk Assessment report and the insights shared at kWh Analytics’ inaugural Broker Council underscore the value of staying informed about the latest trends, challenges, and opportunities in the renewable energy insurance market. As the industry continues to evolve, close collaboration between brokers, sponsors, underwriters, and other stakeholders will be essential to effectively manage risks and drive the sustainable growth of the sector.

Read the 2024 Solar Risk Assessment here: https://www.kwhanalytics.com/solar-risk-assessment